DraftKings Inc: Addressing Feedback on Our Upgrade

Not surprising there was significant pushback to our DKNG upgrade. The focus was mainly on margins, with incremental questions around timing, multiples, balance sheet, and relative preference. We address each of these points below.

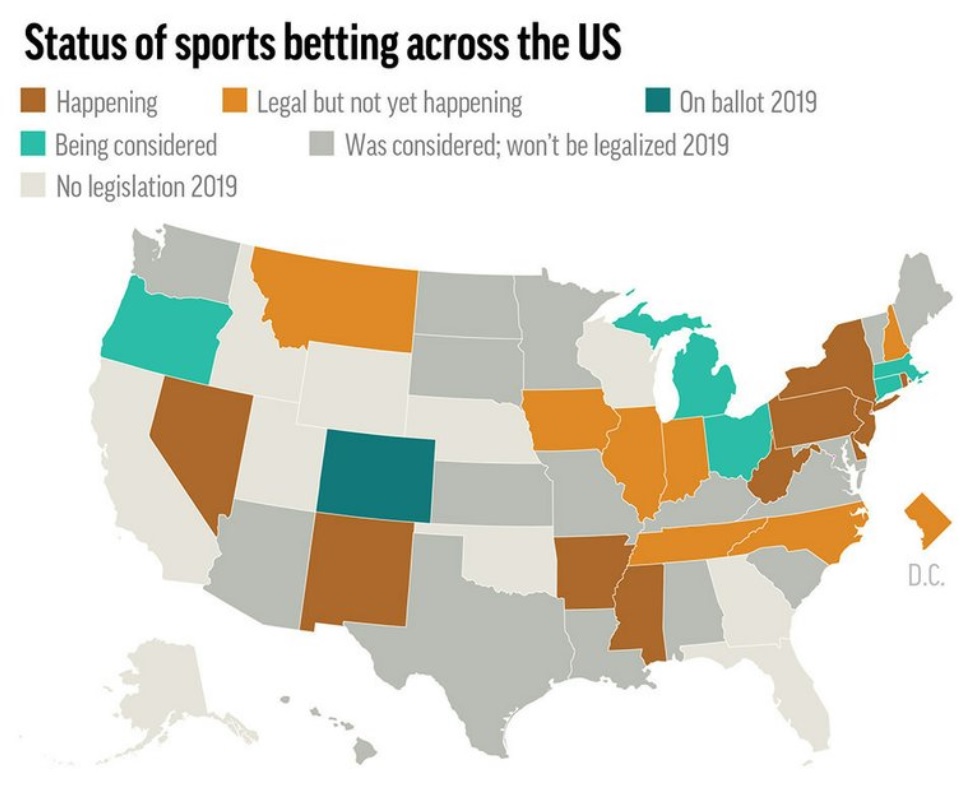

Margins. Investor concerns around margins centered on tax rate increases, marketing spend dissipating, and cost leverage. On tax increases, in 1 inside we show that we have found only 7 examples in the past ~20 years where states have changed existing Gaming tax rates — 4 that increased the rate and 3 that lowered it. Remember that the Gaming industry is typically a very high tax contributor for states, so it generally has political clout. While recent proposals in VA (removing promotion deductions) and HI (55% tax rate) highlight increased risk, these are only proposals right now. Of the 10 states that legalized sports betting in the past year, all (ex NY) have had tax rates of 20% or less (AZ 10%, CT 13.75%, FL 10.00-15.75%, LA 15%, MD 15%, NE 20%, OH 10%, SD 9%, WY 10%). That said, we model avg tax rates of 25% in 2025 vs. 20% in 2021 to bake in potential risk.

On marketing, we expect spend to decrease significantly once the majority of states mature and customer retention becomes more of a focus than acquisition. In our model, we built out a state-by-state waterfall of revenues, marketing and promotional spend to properly reflect this dynamic. While it implies marketing spend drops from ~$1.3B each of the next 3 years to ~$900m in 2025, we see this as fair given there will be fewer new states to be acquiring customers in. Our model reflects promotional spending staying at ~$1.25B in 2025, which implies promo + marketing spend is still 37% of gross revenue in 2025, a very healthy reinvestment rate, in our view. We also went back and calculated DKNG’s 3Q AZ launch CAC based on mgmt’s commentary was ~$200 (2), which we view as encouraging but we would not extrapolate it to other states.

On cost leverage, we model DKNG’s gross profit margins going from 46% in 2021 to 41% in 2022 to 54% in 2025. The drop in 2022 is largely due to the higher NY tax rate. Then going forward, the biggest driver of the improvement should be dissipating promotional spending. Looking at COGS to GGR, we only model it improving 100bps from 2022 to 2025 (3). We expect DKNG’s shift from Kambi to SBTech to continue to drive platform fees lower, increased scale to help lower platform, processing, and rev share fees, but all partially offset by higher taxes. For EBITDA margins, we model Product and Tech spend growing at a 10% ’21-25e CAGR and G&A at ~5%, compared to revenue growing at 38%.

Timing. As we had highlighted as recently as 1/18/22 that the near-term catalyst path for US sports betting & iGaming remained risky, we received numerous question on why the upgrade now? For one, DKNG stock fell 17% from 1/17/22 to our 1/26/22 upgrade, making valuation more compelling. For two, the more investors we spoke to, the clearer it became that consensus was extremely bearish the near-term catalyst path, so any positive surprise could be a significant value driver. We see a chance that when DKNG reports on 2/18, if it guides the Street EBITDA expectations down from $(550)m to our $(800)-(900)m, the stock may actually trade up as it removes the overhang and is likely the trough.

Multiples. There is still a debate in the market on what the best way to value the company is. As we outlined, we believe that using a multiple on 2025 EBITDA using comps’ current 2025 multiples while backing it up with two DCFs is the best way. This reflects the true cash flow of the business, and our upside is driven by having a more bullish view on margins than the market. We did get investor support for our near-term downside case view that DKNG likely would not fall below 3x forward revenue. On our 2023e revenue and assuming its current cash position is burned, that would imply $15, or ~27% downside (4).

Balance Sheet. Some investors were concerned about DKNG’s balance sheet and the potential need to raise capital near-term. While we model DKNG raising capital in 2023/24, we don’t see this as a major near-term risk. We estimate the company will have $2.3B of cash at YE21, and 2022 will be its peak investment year at $1B, which still leaves it with $1.3B of cash at YE22. We model negative operating FCF of ~$500m in 2023, and $250m of taxes paid to tax settle its last LTIP, which may or may not happen. If DKNG wanted to be aggressive, it could still not raise capital in 2023. Hence, we think if a capital raise is needed, DKNG can be patient. However, we acknowledge if CA legalizes OSB, this could accelerate this timeline to 2023.

Relative Preference. Several investors pointed to having a relative preference for other operators like Flutter (Fanduel), MGM or Entain (BetMGM), CZR, or PENN to play US online sports betting relative to DKNG. We think this is fair feedback and we are OW FLTR, ENT, and CZR. We are concerned BetMGM loses market share, and PENN’s Canada (Ontario launches 4/4) share doesn’t live up to expectations. We view DKNG as the pure play on US sports betting / iGaming, with the most negative sentiment, and hence see a greater opportunity to be a contrarian with it.

Prior report: DraftKings Inc: Too Big an Opportunity to Ignore; Upgrade to Overweight (26 Jan 2022).

Online sports betting sites score as NFL season gets under way

BOSTON (Reuters) - Top online sports betting servi...

Half of US offers legal sports betting as NFL season begins

EAST RUTHERFORD, N.J. (AP) — More than half of the...

William Hill Sportsbook Officially Opens at Capital One Arena in Washington, D.C.

WASHINGTON, May 26, 2021 /PRNewswire/ -- Marking a...

Sports betting is days away from becoming legal in Indiana

INDIANAPOLIS (AP) — Sports betting is days away fr...

William Hill US and Mescalero Apache Tribe Announce New Sports Book at Inn of the Mountain Gods Resort & Casino in New Mexico

LAS VEGAS (June 24, 2019) – William Hill US, ...

{kind=link}