SRAD is the largest data distributor in the high-growth global sports betting market, which drives our 25% ’20-’23e rev and ~30% EBITDA growth forecast. We believe SRAD’s quality warrants a premium growth-adjusted multiple vs. pure-play comp GENI. As a result, we initiate on SRAD at OW and $27 PT.

We initiate coverage of SRAD with an Overweight rating and $27 price target, implying 15% upside. We see four key positives. SRAD 1) has significant exposure to the high-growth global sports betting market, which we see growing 12% per year from ’20-23e; 2) is the scaled leader (~40% market share) in the concentrated B2B sports data distribution sector (the only true comps are StatsPerform, Genius Sports, IMG Arena, BetConstruct); 3) has diversified, recurring revenue streams (78% subscription-based) that provide predictability to cash flow generation; and 4) has a proven scalable high-margin (~50% 2020) business internationally that should translate to higher consolidated margins over time as its more nascent (including US) businesses mature.

We think a multiple comparable to peer Genius Sports (GENI), as well as similar growth SaaS stocks is justified. SRAD has a pure-play sports betting data comp trading in the US market already, GENI. While Sportradar’s existing scale (>3x GENI’s 2020 revenue) means it will likely grow slower (consensus forecasting GENI 42% ’20-23e rev CAGR vs. our 25% SRAD forecast), we believe that SRAD deserves a quality premium. SRAD is the market leader by some distance, has a more diversified customer mix, a much larger sporting event portfolio (600k events vs. 240k), and substantially higher EBITDA margins (19% vs. 12%). After considering all these factors, we value SRAD at 8x ’23e EV/sales for our base case, only a modest discount to GENI (9x) on an absolute basis and a premium to GENI on a growth-adjusted basis (we value SRAD at 0.31x EV/sales/growth, close to SaaS comps, vs. currently 0.27x and GENI 0.22x). Our regression of expected 2020-23e growth vs. all comps (18) would justify an 11x ’23e revenue multiple, but we apply a discount due to the risks outlined below.

We see four key risks: 1) SRAD serves as an intermediary between sports leagues (concentrated domestically) and sportsbooks (also typically concentrated), though our channel checks suggest both appreciate the role it plays; 2) we assume SRAD grows ~2x the sports betting industry, driven by cross-selling of non-core data products (primarily AV/streaming, digital ads, managed betting/trading services); 3) sports rights cost inflation could be higher than expected (NBA and MLB rights come due in 2-3 years); and 4) while competition is concentrated, GENI is competing on price and IMG Arena just improved its offering.

Attractive risk-reward ($57 bull case implies 144% upside / $14 bear case implies 41% downside). Our base case assumes SRAD grows revenue from €405m in 2020 to €798m in 2023e, and EBITDA from €77m to €167m. In our bull case, we assume revenue grows at a 35% CAGR in 2020-23e, with EBITDA margins reaching 25% (vs. 21% in our base case). We use 8x 2023e Sales to arrive at our base case. Our bull case comps are high-growth SaaS stocks (Zoominfo, Coupa, BigCommerce, and Atlassian), which trade at 20x 2023e Sales on average. We use a 14x multiple (lower-end of bull case Software comps) to arrive at our $57 bull case, which implies 144% upside. In our bear case, we assume revenue grows at a 15% CAGR in 2020-23e and EBITDA margins of 15%. Our bear case comps are lower growth tech platforms, GoDaddy and McAfee, which are trading at 4.2x 2023e Sales on average. We use 5x 2023E Sales to arrive at our $14 bear case, which implies 41% downside.

NFL Brings On-board Sportradar

Compared with other U.S. sports leagues, the NFL h...

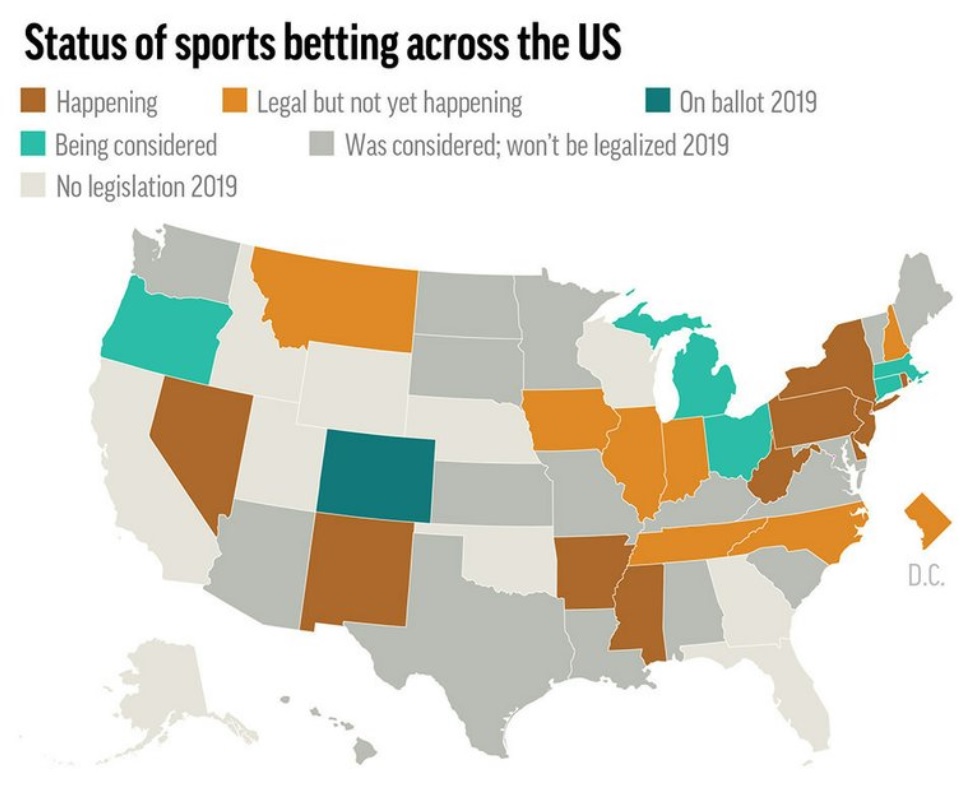

Half of US offers legal sports betting as NFL season begins

EAST RUTHERFORD, N.J. (AP) — More than half of the...

William Hill Sportsbook Officially Opens at Capital One Arena in Washington, D.C.

WASHINGTON, May 26, 2021 /PRNewswire/ -- Marking a...

Nasdaq dealing in Sports Betting

Nasdaq Inc. is lending its technology an...

Sports betting is days away from becoming legal in Indiana

INDIANAPOLIS (AP) — Sports betting is days away fr...

{kind=link}