Better Collective has reported a “transformational” 2025, delivering its highest-ever EBITDA while advancing structural efficiencies and investing in AI-driven products including Playbook and FanReach.

Despite external headwinds, the group closed the year with record deposit values and a standout Q4 EBITDA before special items of €37 million, underlining continued operational momentum. Looking ahead, management has issued 2026 guidance forecasting organic revenue growth of 7–12% and EBITDA growth of 8–18%, supported by disciplined capital allocation and annual share buybacks of €40 million.

With strategic priorities sharpened and the upcoming FIFA World Cup expected to drive engagement across its global sports media portfolio, the company enters 2026 positioned to sustain growth and strengthen its leadership in digital sports media.

Regulatory release no. 12/2026

Jesper Søgaard, Co-founder & Co-CEO of Better Collective, comments:

“2025 was a transformational year for Better Collective. Despite some significant external headwinds, we stayed disciplined and structurally strengthened our business while investing in key AI innovations such as Playbook and FanReach that will help drive our future growth. I am pleased to report that we ended the year with our highest EBITDA ever, a milestone that speaks directly to the hard work of my colleagues across the globe. We have carried that momentum into 2026 with a laser-sharp focus on our top priorities, combined with the upcoming FIFA World Cup in men’s soccer, which stands as a massive opportunity for our business.”

Q4 2025 highlights:

- Q4 revenue 94 mEUR

- -2% year-over-year

- +2% year-over-year in constant currencies

- Q4 EBITDA before special items 37 mEUR

- The highest EBITDA before special items ever recorded in a quarter

- Value of deposits all time high 820 mEUR

2026 financial guidance

- Organic revenue growth 7-12%

- EBITDA before special items growth 8-18%

- Annual share buybacks of 40 mEUR

- Net debt to EBITDA before special items below 3x

2027-2028 financial guidance

- Organic revenue growth

- EBITDA before special items margin of 35-40%

- Continued strong cash conversion

- Net debt to EBITDA before special items below 3x

The company collected consensus from analysts following the company can be found on Better Collective’s website here.

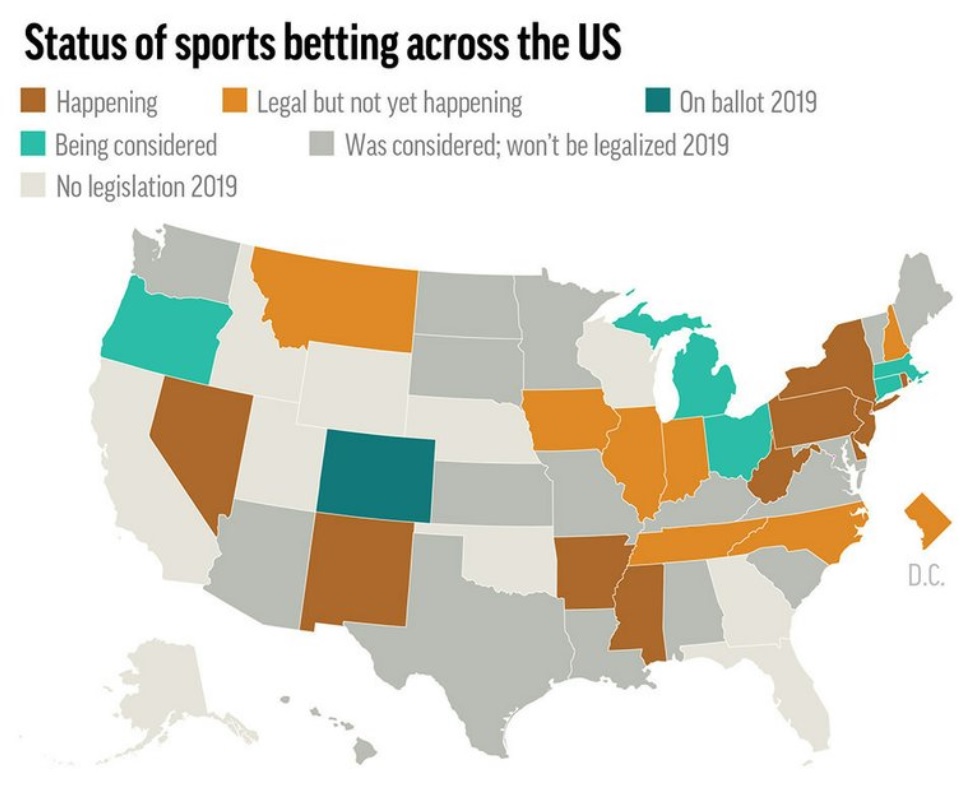

Half of US offers legal sports betting as NFL season begins

EAST RUTHERFORD, N.J. (AP) — More than half of the...

William Hill Sportsbook Officially Opens at Capital One Arena in Washington, D.C.

WASHINGTON, May 26, 2021 /PRNewswire/ -- Marking a...

William Hill US and Mescalero Apache Tribe Announce New Sports Book at Inn of the Mountain Gods Resort & Casino in New Mexico

LAS VEGAS (June 24, 2019) – William Hill US, ...

Sports betting is days away from becoming legal in Indiana

INDIANAPOLIS (AP) — Sports betting is days away fr...

Caesars now operates sportsbooks in seven states at nearly 30 venues

29 Sports Betting Locations Across Seven States by...

{kind=link}